For Smart People Over 45 Who Are Ready for a Different Retirement Plan

For Smart People Over 45 Who Are Ready for a Different Retirement Plan

You Already Know 7% Won't Get You There.

Here's the Math That Will.

The education system that shows people 45+ how one asset class creates a completely different retirement equation. No Wall Street. No expensive advisors. No pretending the old system will suddenly start working.

It's 2am. You're Sitting at the Kitchen Table. Again.

The laptop screen is the only light in the room. On it, a retirement calculator you've already run three times tonight. Because maybe you entered something wrong. Maybe there's a number you missed.

There isn't.

$65,000 in your 401(k). After twenty years of contributing. Twenty years of following the rules. Twenty years of choosing the "recommended" funds, maxing out what you could afford, doing everything the financial advisor told you to do.

You need $1.8 million to retire comfortably at 65.

You have 14 years. And sixty-five thousand dollars.

You went through a divorce that split your savings in half. You skipped vacations to contribute more. You survived 2008 while your advisor told you to "stay the course."

The retirement calculator can't see any of that. It only sees numbers.

And right now, the numbers say: at 7% returns, you'll have roughly $340,000 by 65. About 20% of what you need.

The numbers need a different vehicle to get where you need to go.

You close the laptop. But you already knew. You've known for a while now. That's the weight you carry. The quiet hum of anxiety that never fully goes away. The thing you don't talk about at dinner. The reason you pour that second glass of wine at 9pm. The number that sits in the back of your mind while you're smiling at your grandkids, thinking: will I be a burden to them?

If you're reading this, you probably know that feeling.

Maybe your numbers are different. Maybe you have more saved. Maybe less. But the story is the same: at 7% returns, the math doesn't work. And every financial advisor you've ever talked to has given you the same answer.

Save more. Cut back. Hope.

That's not a plan. That's a prayer.

And you're done praying.

Here's What Nobody Told You: It Wasn't Your Fault.

Read that again. It was not your fault.

You didn't fail at retirement savings. The system failed you.

Let me show you how.

In 1971, the U.S. dollar was disconnected from gold. Money became something that could be printed without limit. And print they did. Forty percent of all U.S. dollars in existence were created in just the last four years.

Think about that. Almost half of all dollars ever created. In four years.

What does that mean for you?

It means your "safe" savings account is bleeding purchasing power every single year. The government tells you inflation is 2 to 3 percent. But go to the grocery store. Fill up your gas tank. Look at your health insurance premium. Pay your property taxes.

Does that feel like 2 to 3 percent?

Real inflation (the cost of the things you actually need in retirement) runs 7 to 10 percent. Your $50,000 in savings? At 7% real inflation, that has the purchasing power of about $25,000 in just ten years. You didn't spend a penny. The value just vanished.

This is the invisible theft. It's happening right now. While you're reading this sentence.

And here's the part that should make you angry.

The wealthy don't keep their money in savings accounts. They never have. They keep it in assets that outpace inflation. Real estate, businesses, scarce commodities. They know the game. They've always known.

You were playing by rules designed for a different era. An era when saving actually worked. When compound interest at 7% was enough. When a pension was waiting for you at the end.

That era ended decades ago. Nobody told you.

Until now.

Two Types of Assets. One Decision.

Your old retirement plan isn't broken. It's obsolete. There is a new one. And the window to use it is open right now.

Preservation Assets

Bonds. Target-date funds. Most 401(k) options. They earn 4 to 7 percent. These are designed for people who already have $2 million and just need to protect it. That's not you.

Growth Assets

Designed for accelerated growth. More volatile, yes. Some years up 60%. Some years down 30%. But they have the mathematical potential to compress 30 years of growth into 10 to 15.

Think of it this way. You're in a race against time. And you've been driving a minivan. It doesn't matter how hard you press the gas. The vehicle has a speed limit. Your financial advisor put you in a minivan and told you it was a Ferrari.

You don't have a savings problem. You don't have a discipline problem.

You have an obsolete vehicle problem.

And right now, there is a completely different retirement math available to you. Not the old 7% math. Not the "save more and hope" math. A new math, built on an asset with a fixed supply in a world of unlimited dollars. I call it The New Retirement Math.

The Asset Is Bitcoin.

I know. Stay with me.

Before you close this page, let me give you the entire argument in one sentence:

21 million is less than infinity.

That's it. That's the whole thesis.

There will only ever be 21 million Bitcoin. That's not a company promise. It's coded into the software. Unchangeable. Permanent. Meanwhile, dollars have no limit. The government can create as many as they want, whenever they want, for whatever reason they want. And they do.

Unlimited dollars chasing a limited asset. What happens to the price?

That's not speculation. That's supply and demand. The same economics you learned in high school.

This is The New Retirement Math in action. Right now, Bitcoin sits where the internet was in 1997 on its adoption curve. Institutions are just beginning to allocate. ETFs just launched. Governments are starting to accumulate reserves. The gap between where it is and where adoption curves say it's going creates a mathematical window that won't stay open forever.

Now here's where it gets interesting for someone in your situation.

Bitcoin has historically averaged returns that make your 401(k) look like a parking lot. Even conservative forward projections suggest 20%+ annually for the next 15 to 20 years.

in 14 years

in 14 years

That's not a typo. That's the difference between a preservation asset and a growth asset.

They Had the Same Fear. They Did It Anyway.

"But it crashes. It's volatile. It's risky." Let me reframe that through the people who had the exact same fear.

She thought Bitcoin was "for tech people." Three times she talked herself out of it. Then she ran her retirement numbers: $180,000 saved, needed $1.2 million. At 7%, she was going to have about $380,000 by 65. A third of what she needed. When she saw that math, the question changed. It wasn't "Am I tech-savvy enough?" anymore. It was "Can I afford NOT to learn this?" By week three, she understood Bitcoin better than her 25-year-old nephew. First purchase took 20 minutes on a Saturday morning.

Gary wasn't interested in Bitcoin. At all. His son kept bringing it up at family dinners, and Gary kept shutting it down. Then Gary ran his retirement numbers. Really ran them. Not the ones his advisor showed him. The real ones, adjusted for real inflation. The gap scared him. Enough to listen. Not to his son's hype. To the math. His flip phone didn't stop him. He did his research on a library computer. He opened an account on his desktop at home. His son helped with the initial setup, and after that, Gary managed it himself. He told me, "This isn't about being tech-savvy. It's about being honest with yourself about the math." Gary's flip phone sits right next to a portfolio that's done more in 18 months than his 401(k) did in 10 years.

Never finished one. She finished J. Scott's book. Because it wasn't about becoming a trader or a tech expert. It was about understanding math. And math, she could do.

He sat on this page for three days. Then he sent 14 questions by email. He joined. Three weeks later he wrote back: "You were the first person who told me I was right to be angry at the system, and then actually showed me what to do about it."

Here's What You Need to Understand About "Risk"

Visible Risk

The volatility you can see. Bitcoin goes up 60%. Then drops 30%. Headlines scream. Pundits panic. It feels scary.

Invisible Risk

The erosion you can't see. Your purchasing power declining 7 to 10 percent every year. Your retirement date getting further away with every passing month. Nobody screams about it. But it's gutting your future right now.

If you're 45+ and your current plan isn't working, staying in 7% assets isn't the safe choice.

It's the riskiest thing you can do. Because it guarantees the math never works.

At 58, I Was You.

My name is J. Scott MacMillan. I live in Montana. I spent years as a network engineer building invisible systems that make everything else work. Later, as a corporate trainer, I discovered something unexpected: the same architectural principles that govern networks also govern financial markets and the monetary system itself.

That's when I started seeing the map behind the map.

At 58, I sat down and ran my own retirement numbers. And the math didn't work. Not a little off. Way off. I had a financial advisor managing my IRA in the standard 60/40 mix. And when I finally looked at the truth, I realized 7% returns weren't going to get me where I needed to go.

So I did what any engineer would do when the system stops working. I found the flaw. The financial architecture had changed. The rules had shifted. And I'd been playing by guidelines designed for a monetary system that no longer exists.

I spent two years studying the economics of scarce assets, market cycles, and monetary policy. Not from YouTube gurus. From the fundamentals. I discovered The New Retirement Math. I acted on it. And everything changed.

For six years now, I've guided people through the intersection of mindset transformation and strategic wealth building. I don't offer motivation. I offer clarity.

The FREEDOM Framework

Seven steps from fear to financial clarity.

The Great Catch-Up Investing System

Your Complete 18-Module Financial Transformation System

Here's What Happens in 6 Weeks

The complete education system built for people 45+ who need a new retirement path.

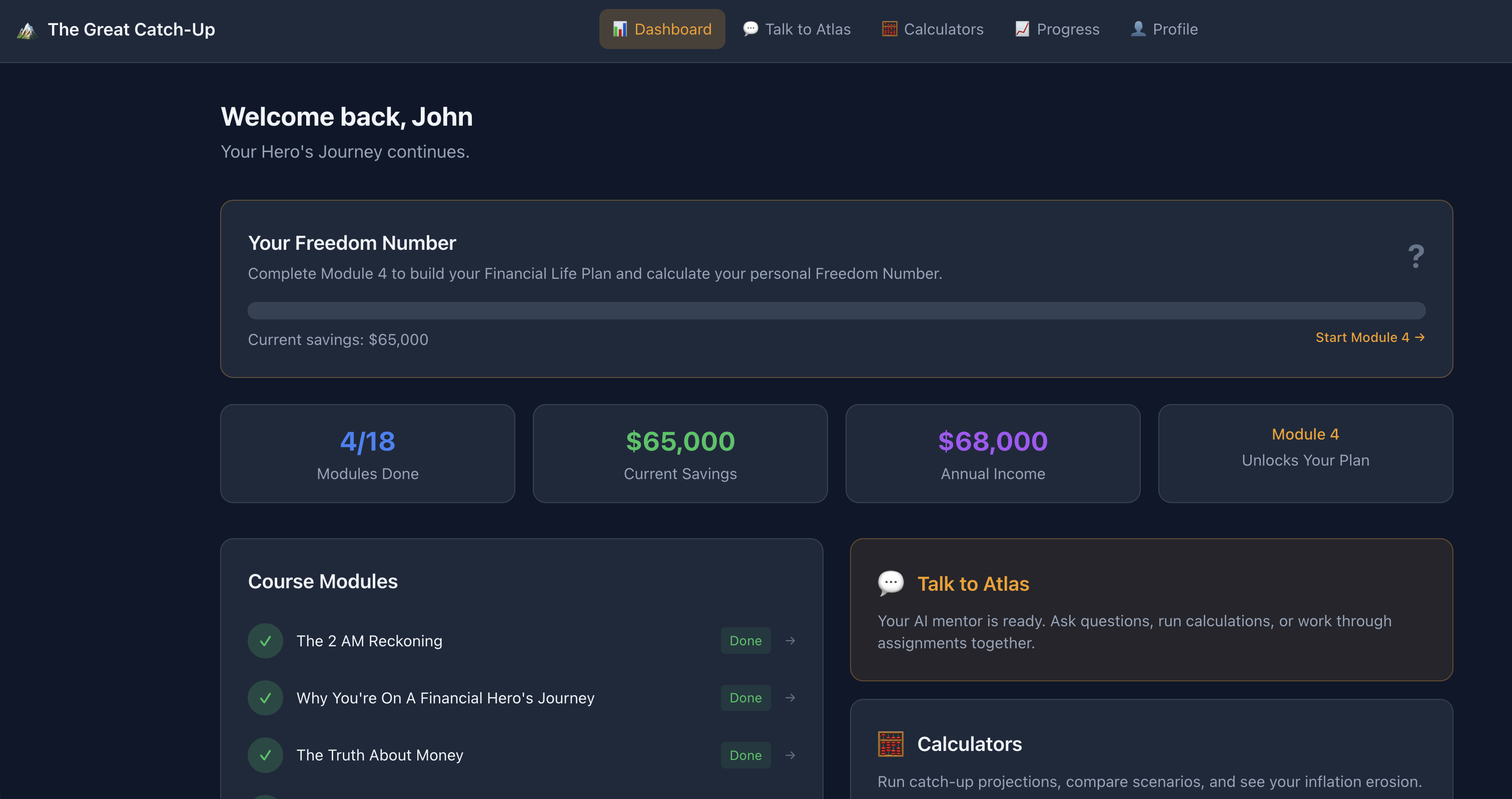

Your Freedom Number

This is the number that changes everything. Your exact retirement target, calculated for your specific situation. Not a vague "save more" lecture. Not a range. YOUR number. The dollar amount that means "enough." Most people carry around this shapeless anxiety because the fear has no edges. After Week 1, it has a number. And numbers have solutions.

The Truth About Money

Why the system is designed to erode your savings. Real inflation versus what they tell you. How 40% of all dollars were printed in four years. Why traditional advice became obsolete the moment the dollar left the gold standard. After this week, you'll understand exactly why your old plan stopped working. And for the first time, you'll know it wasn't your fault. Not as a feel-good platitude. As provable, mathematical fact.

The One Asset

A complete Bitcoin education built for people who "aren't tech people." The supply-and-demand math. The institutional adoption trend. Why it must appreciate over time based on economics, not hype. And why The New Retirement Math exists right now.

Your Personal Strategy

How to build a portfolio designed for your specific timeline and comfort level. Bitcoin allocation. Tech/AI stocks for diversification. Bitcoin ETFs for your existing 401(k) and IRA. Plus: your complete volatility playbook. What to do if Bitcoin drops 20%, 40%, or 60%. Historical data showing every major crash and the recovery timeline. A decision tree for every scenario. Because the question isn't IF it drops. The question is whether you have the framework to hold through it.

Your First Move

Step-by-step implementation. How to buy Bitcoin safely. How to store it. How to set up recurring purchases. How to add Bitcoin ETFs to your retirement accounts. Everything broken down into 15-minute steps. Twelve of them. You could do this in a single weekend.

Your Path Forward

Long-term strategy. When to hold. How to think about volatility when headlines are screaming. What the next 4 to 15 years likely look like based on market cycles and historical data. How to sleep well on a Tuesday when the market drops 15%.

Here's Exactly Where You'll Be at Every Stage

Your Freedom Number calculated

First investment made

Portfolio structure complete, recurring purchases automated

First rebalance checkpoint (what to look for, what to adjust)

Progress check against your Freedom Number projection

Full strategy review, next phase planning

Compounding phase (this is where the math gets exciting)

Plus: 6 Weeks of Live Zoom Calls

You. Me. Your questions. Every week. No question is too basic. No concern is too simple. Linda's first question on the Zoom call was: "What's an app?" No joke. And nobody laughed. Because everyone on the call was in the same boat.

This is education, not financial advice. I show you my system, my research, my framework. What you do with it is your decision. But you'll make that decision from a place of clarity. Not confusion. Not fear.

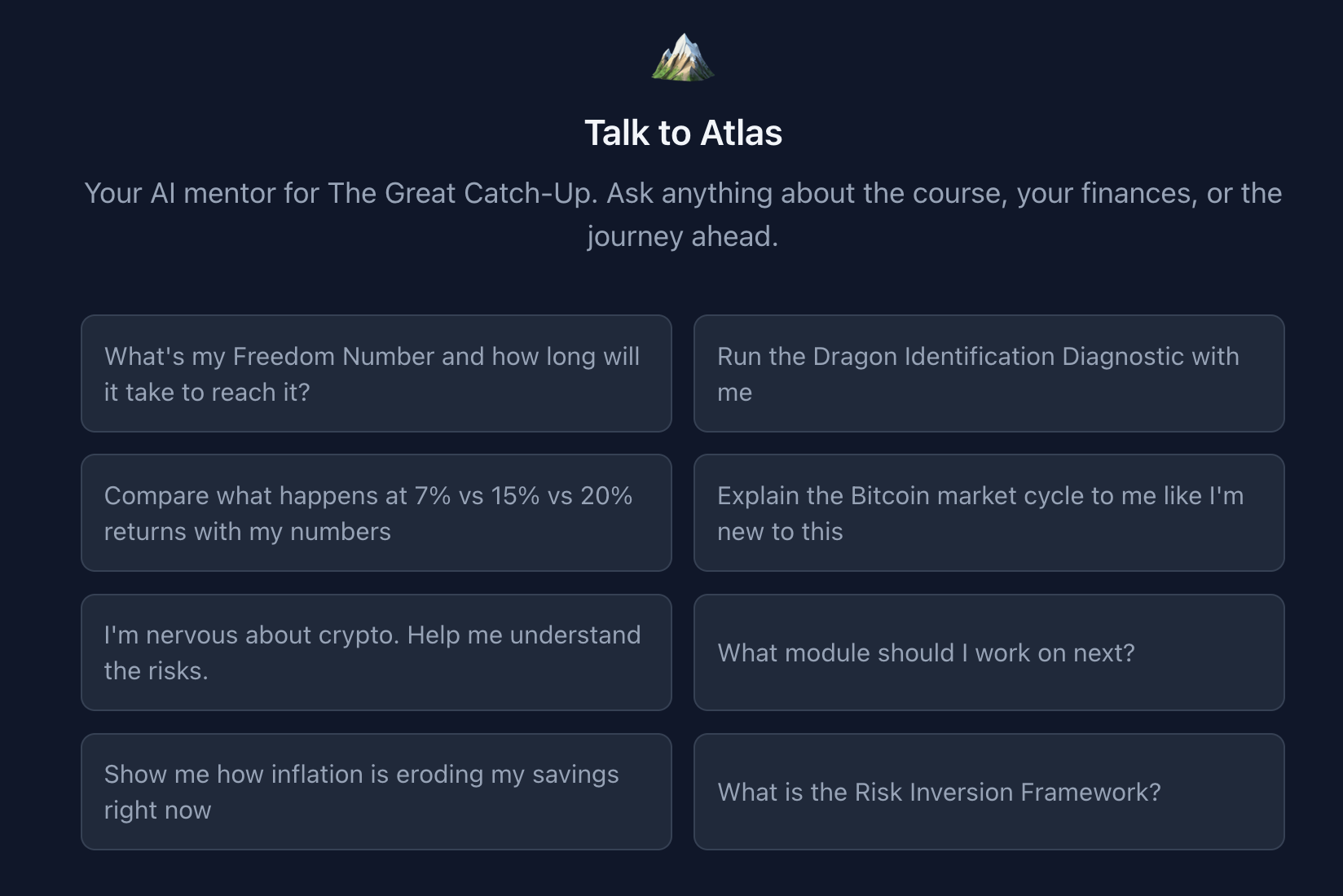

Meet Atlas: Your Personal Great Catch-Up Mentor

This is where The Great Catch-Up becomes something nobody else offers. Atlas isn't a chatbot that gives generic answers from the internet. He's trained on every concept, every framework, every lesson in this entire curriculum.

Knows YOUR Numbers

Tell Atlas your savings, income, and Freedom Number. He runs calculations with YOUR data. "Based on your savings of $63,000 and your Freedom Number of $1.2 million, here's what the math looks like at different return rates." That's YOUR plan coming to life.

10 Coaching Frameworks Loaded

Feeling scared? He'll run the Four Financial Dragons Diagnostic. Thinking the "safe" route is better? He'll walk you through the Risk Inversion Framework. Confused about timing? The Cyclical Positioning System. Struggling with identity? The Identity Threshold Framework.

Available 24/7. No Judgment. Ever.

3 AM and can't sleep because you're worried about money? Atlas is there. Sunday afternoon and you want to run some numbers? Atlas is there. He never judges. He never rushes you. He never makes you feel stupid for asking a question.

Real-Time Calculators in Every Conversation

Built-in calculators that run live during your conversations. Year-by-year projections with your actual numbers. Side-by-side scenario comparisons. Your numbers, calculated in real time.

Think of Atlas as a math tutor and supportive coach all in one. Available whenever you need them. Who never gets tired of your questions.

Tools That Do the Hard Math

Every major concept has a tool that makes you DO the work. Not just read about it.

Balance Sheet Calculator

See every asset and liability. Your complete financial picture for the first time.

Income & Expense Analyzer

Find the "invisible money" hiding in subscriptions and fees you forgot about.

Risk Assessment Tools

Psychological quiz plus mathematical scorer. What you CAN handle vs what you can AFFORD.

Freedom Number Builder

Your exact retirement target. Based on YOUR expenses, YOUR Social Security, YOUR life.

Milestone Map Generator

Breaks your Freedom Number into 5 to 7 achievable milestones so it doesn't feel impossible.

Traditional Advice Calculator

See exactly why 7% can't work. The moment most people realize they need a different approach.

Everything at a Glance

Freedom Number Progress

Visual progress bar showing how far you've come

Module Tracking

Completion percentage, assignments done, milestones hit

Quick Access to Atlas

One click to your AI mentor, calculators, and Dragon Diagnostic

Your Financial Life Plan

Download all assignment responses as one complete PDF

You're Not Buying a Course. You're Getting a System.

The Truth About Where You Stand

No more vague anxiety. Real numbers. Real clarity.

YOUR Number. Not a Generic One.

Not "save a million dollars." YOUR Freedom Number based on YOUR life.

Tools That Do the Hard Math

Interactive tools build your plan step by step.

A Mentor Who Knows Your Situation

Atlas is available whenever you need him. 2 AM included.

Progress You Can See

Track every module, every assignment, every milestone.

Live Calls with J. Scott

Check-ins, accountability, and that personal touch.

You could hire a financial advisor for $200 to $400 an hour who gives you generic advice and sees you once a quarter. Or you could get J. Scott live and Atlas, who knows every framework, has your numbers loaded, and is available at 2 AM when you can't sleep.

Sign Up For The Waiting ListHere's Everything You Get Today

Choose Your Path

Less than your morning coffee. Less than the daily purchasing power your savings are losing right now while they sit in a bank account earning next to nothing. Less than the invisible fee your advisor charges you every single month to keep you in the same funds that got you here.

What the Alternatives Actually Cost

A Bitcoin guru mastermind: $3,000 to $25,000. Most want you trading daily, which is the opposite of what works for your timeline.

A generic Bitcoin course: $297 to $997. They teach trading to 25-year-olds, not allocation strategy to people our age.

Doing nothing for one more year: At least $29,520 in purchasing power erosion on $250,000. Plus the compound growth you'll never get back.

Buying Bitcoin without education: The average person who buys without a framework sells during the first major dip and locks in 30% to 40% losses. On a $50,000 position, that's $15,000 to $20,000 in preventable mistakes.

My Personal 30-Day "Try Everything" Guarantee

Enroll today. Watch the first 4 modules. Do the exercises. Use the calculator. Ask every question. Take the full 30 days.

Week 1 Free-Look

Complete Week 1. If you don't already see your retirement situation differently, email us before Week 2. Full refund. Zero risk.

Sleep-At-Night Promise

If you complete the first four modules and still don't feel confident managing volatility for YOUR situation, get your full refund.

No Stupid Questions (48hr)

Every question gets a thoughtful response within 48 hours. If any question ever goes unanswered longer than that, email J. Scott MacMillan personally.

Anti-Sales Guarantee

If at any point you feel sold to, upsold, or pressured inside the program, full refund. There is nothing else to buy after this.

Honest Assessment

If J. Scott MacMillan looks at your situation and believes this path isn't right for you, he'll tell you directly and refund your investment himself.

Payment Plan Protection

$260 x 2. Same guarantee. Same bonuses. Cancel between payments with one email. Full refund of all payments within the 30-day window.

This is my name on the line. Not a corporation. Not a brand. Me, J. Scott MacMillan. The guy who was 58 and found a new path. If I can't help you see one too, I don't deserve your money. And you keep $1,137 in bonuses. Even if you refund.

Let's Talk About What Happens If You Don't Act.

Not to scare you. To be honest with you.

Every day you wait, inflation erodes roughly $82 of purchasing power on $250,000 in savings. That's $574 per week. $2,460 per month. $29,520 per year. Just from inflation.

That's not speculation. That's math.

And it gets worse. Because it's not just what you're losing. It's what you're missing. Every day this window is open and you're not positioned, you're leaving compound growth on the table. The kind of growth that turns $65,000 into $1.2 million. But only if you start.

The math of doing nothing isn't neutral. It's negative. Every single day.

48-Hour Fast-Action Bonus

Personal 30-minute Strategy Session with J. Scott MacMillan (normally $500).

We'll look at your specific numbers, your specific situation, and you'll get clear on what your options are. After 48 hours, this disappears. I can only do 20 of these per cohort, and they go fast.

One year from today, which version of you do you want to be?

The version who read this page, understood the math, felt the pull, and decided to wait? Who's still running that retirement calculator at 2am, still carrying the weight, still telling yourself "someday"?

"Today. Not someday. Today."

Linda chose at 57. Gary chose at 54. Diane chose at 52. Mark chose at 58.

None of them felt ready. Every single one of them was scared. And every one of them said the same thing afterward:

"I wish I'd done this sooner."

Frequently Asked

You've Been "About to Do Something"

for a While Now.

Something in you already knows that 7% and "stay the course" isn't going to work. Something in you already knows the old plan is obsolete. The question was never whether this path makes sense. You've seen the math. The question is whether today is the day you stop saying "someday."

$497 for the Founding Member spot. $260 x 2 if you need the payment plan. 30-day guarantee. Keep the bonuses no matter what. Plus a personal Strategy Session if you act in the next 48 hours. And me. Personally. For 30 days. In your corner.

Because I've been at that kitchen table at 2am. And I know the way out.

The Great Catch-Up is an educational program. It is not financial advice, and J. Scott MacMillan is not a licensed financial advisor. All investment decisions carry risk, including the risk of losing your entire investment. Past performance of any asset, including Bitcoin, does not guarantee future results. You should consult with a qualified financial professional before making any investment decisions. The income and return examples used in this material are for educational illustration purposes only and are not promises or guarantees of actual results. Individual results will vary based on a wide range of factors including but not limited to individual effort, market conditions, and economic factors beyond anyone's control.